May 14, 2026

- AI Technology

- Interior Design

How AI-First Insurers Can Use 3D Property Data to Transform Home Claims | VirtualSpaces

Hemanth Velury

CEO & Co-FounderHow AI-First Insurers Can Use 3D Property Data to Transform Home Claims Assessment

When a homeowner files a property damage claim, the insurer faces a question that sounds simple but rarely is: what did this home actually look like before the damage?

Right now, the answer is almost always inadequate. A handful of old photographs. A site visit report from an assessor who never saw the property pre-loss. A floor plan on paper, if the owner kept it. Sometimes, nothing.

This documentation gap is where claims fraud hides. It is also where legitimate claims get delayed, disputed, or undervalued, not because of bad faith, but because there was never a reliable spatial record of the property to begin with.

A new generation of AI-first insurers has already understood that better data produces better outcomes. What they have not yet fully operationalized is the most important data type of all: verified, photorealistic, spec-accurate spatial records of the homes they insure. AI 3D visualization is the technology that makes this possible, at scale, today.

The Insurers Already Thinking This Way

The shift toward data-native insurance is not theoretical. It is happening in real companies with real capital behind it.

Lemonade has built its entire operating model on AI-driven underwriting and claims processing. Its AI claims bot, Jim, can approve and pay certain claims in seconds, but only because it has structured data to work with. The constraint Lemonade faces, like every residential insurer, is that the underlying property data is still largely unverified and un-spatial.

Kin Insurance goes further by pulling in satellite imagery, aerial data, and property records to underwrite homes without requiring agent visits. Kin's model is explicitly about using external data signals to understand a property's risk profile before a human ever sets foot on it. Spatial interior data is the logical next layer: what is inside the home, how it is configured, and what it would cost to replace.

Fidelity National Financial, through its title and property data businesses, sits on one of the largest repositories of real estate records in the United States. As that data increasingly moves toward AI-driven analysis, the addition of verified interior spatial records becomes a natural extension of what the company already does.

Each of these companies is building toward the same destination: insurance underwriting and claims that are grounded in verified, queryable property data rather than self-reported declarations. Tools like Foursite and Remodroom by VirtualSpaces are precisely the infrastructure layer that closes the gap between exterior property data and interior spatial reality.

The Core Problem: Insurers Are Still Working Blind on the Inside

Kin can tell you a roof's age from satellite imagery. But it cannot tell you whether the kitchen has custom cabinetry or laminate finishes. Lemonade can process a claim in seconds if the data is clean, but if the pre-loss condition is disputed, the speed advantage evaporates. Fidelity knows everything about who owns a property; it knows very little about what the interior actually looks like.

This is the structural blind spot in residential property insurance globally: the exterior is increasingly well-documented, the interior almost never is.

The consequences are predictable:

-

Fraud vulnerability: Without a verified baseline, distinguishing genuine damage from inflated or fabricated claims depends on assessor judgment, not data

-

Assessment inconsistency: Two assessors visiting the same damaged property regularly produce materially different valuations

-

Delay and dispute: When pre-loss condition is unclear, every claim costs more to resolve and carries higher litigation risk

-

Mispriced risk: Policies covering high-finish homes are often priced the same as standard-finish homes because the insurer cannot verify the difference at inception

What AI-first insurers need is a spatial baseline: a verified, photorealistic, timestamped 3D record of a property's interior, captured at policy inception and queryable at any future point.

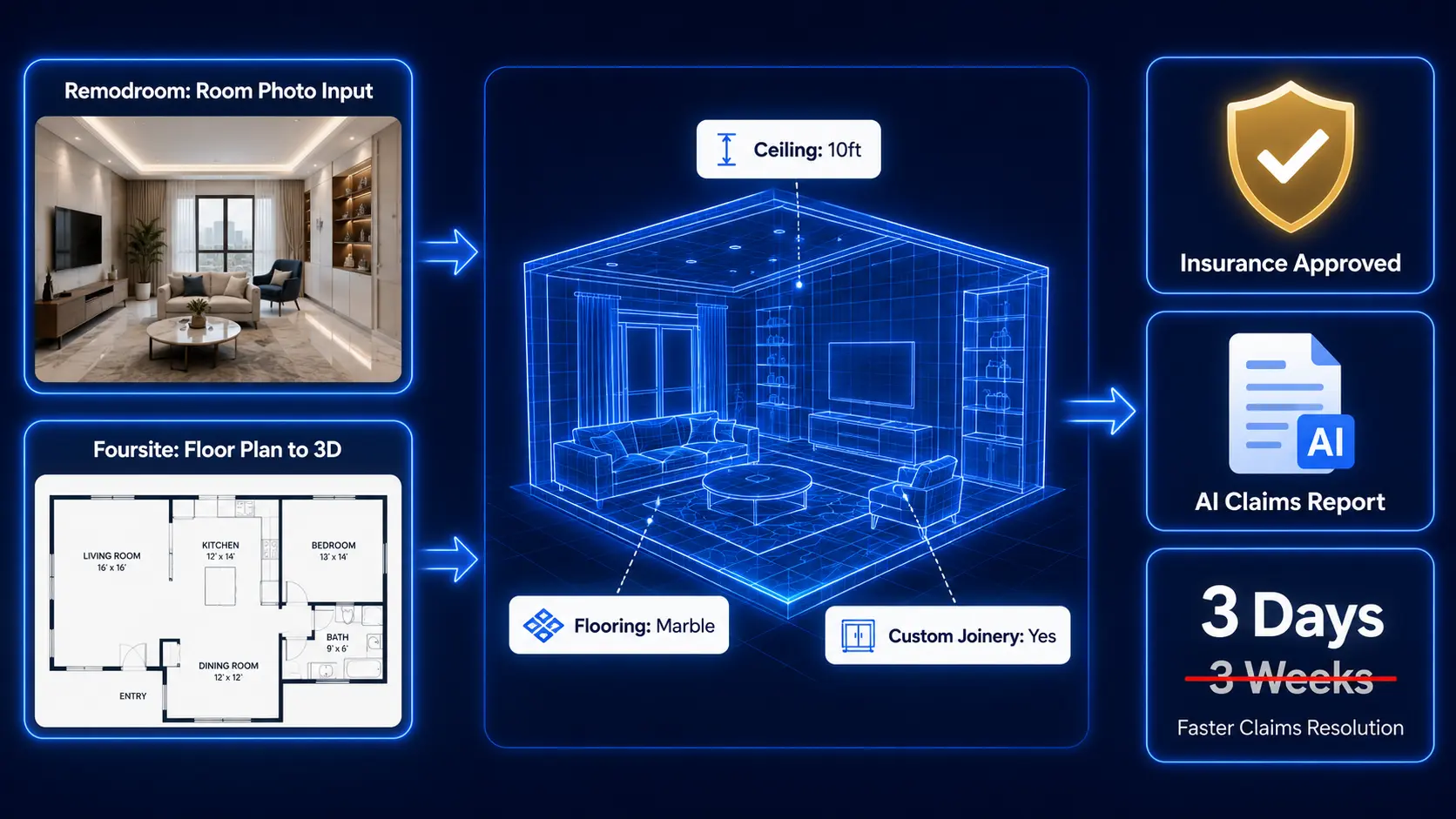

What Foursite and Remodroom Make Possible

Foursite by VirtualSpaces converts 2D floor plans and architectural blueprints into photorealistic AI 3D interior renders in minutes. The output is geometrically faithful: it reads actual room dimensions, wall relationships, door placements, and fixture positions from the source blueprint. The result is a spec-accurate, navigable 3D walkthrough of a property that did not previously exist in digital form.

Remodroom works from photographs. A homeowner uploads a photo of any room and Remodroom generates a photorealistic, spatially-aware 3D record of that space, preserving actual geometry while structuring the visual data into a queryable format. No architect required. No surveyor required. Just a smartphone photograph.

Together, they create two entry points for building an interior spatial baseline:

| Scenario | Input | Tool | Output |

|---|---|---|---|

| New home, plans available | 2D floor plan / blueprint | Foursite | Spec-accurate 3D walkthrough |

| Existing home, photos only | Room photographs | Remodroom | Photorealistic 3D room record |

| Post-renovation update | Updated plans + new photos | Foursite + Remodroom | Revised spatial baseline |

| Claims assessment | Post-loss photographs | Remodroom | Structured damage documentation |

This is infrastructure that any AI-first insurer can plug into their existing data pipeline. The inputs are documents homeowners already have. The outputs are structured spatial records that an AI claims engine can actually use.

Three Operational Use Cases for AI-First Insurers

Pre-Policy Spatial Documentation at Inception

The most powerful intervention is the simplest: build spatial baseline capture into the policy onboarding flow.

When a homeowner applies for residential property insurance, they already submit photographs, a property valuation, and sometimes a floor plan. None of these create a spatially accurate, queryable record. A floor plan to 3D conversion via Foursite, or a room-by-room photographic record processed through Remodroom, gives the insurer something entirely different, a verified spatial snapshot of the property at inception.

The onboarding workflow becomes:

I. Homeowner submits floor plan PDF or room photographs during application

II. Insurer runs inputs through Foursite or Remodroom to generate 3D spatial records

III. Records are timestamped, stored, and linked to the policy file

IV. At any future claim, the pre-loss baseline is immediately available for comparison

For Lemonade, this feeds directly into Jim's claims processing capability: instead of relying on self-reported descriptions of pre-loss condition, the AI works from a verified spatial record. For Kin, it extends their exterior data model into the interior. For Fidelity, it becomes a new layer of property intelligence attached to every policy in their book.

AI-Driven Pre/Post Claims Comparison

With a pre-loss spatial baseline in place, the claims assessment process changes structurally. The assessor's job shifts from reconstruction to verification.

Current State (industry standard):

-

Assessor visits damaged property

-

Manual documentation: 1-3 days

-

Report preparation: 3-5 days

-

Dispute resolution, if any: weeks to months

-

Average full cycle: 3-8 weeks

With Spatial Baseline:

-

Homeowner submits post-loss photographs

-

Remodroom converts photos to structured 3D record: hours

-

AI compares pre-loss and post-loss spatial models: hours

-

Preliminary damage scope report generated: same day

-

Assessor visit focused on verification, not discovery

-

Average full cycle: days

The damage scope report produced by this process identifies which elements were affected, what their pre-loss specification was, and what replacement costs are based on current material pricing. This is the kind of structured output that Lemonade's AI infrastructure is built to consume, and that Kin's underwriting model can use to close the loop between risk assessment and claims outcome.

Fraud Detection Through Spatial Inconsistency Analysis

Property insurance fraud costs the global insurance industry an estimated $80 billion annually. A significant portion involves interior misrepresentation: claiming damage to finishes or fixtures that were never present, inflating the quality of interiors, or fabricating high-value elements after the fact.

A pre-loss AI 3D visualization record makes most of these fraud vectors structurally difficult to execute:

-

A claim for destroyed imported marble flooring is immediately compared against a pre-loss record showing ceramic tile

-

A claim including a custom home theater system is checked against a baseline that shows a standard living room

-

A claim inflating room count is verified against a geometrically accurate floor plan record

The deterrence effect compounds over time. When policyholders know a verified spatial record exists at inception, the incentive to inflate claims decreases before a claim is ever filed. This is not just a claims improvement, it is an underwriting quality improvement that reduces loss ratios at the portfolio level.

The Underwriting Angle: Spatial Data as a Pricing Signal

Beyond claims, interior spatial data has significant implications for how AI-first insurers price residential risk.

Currently, residential property insurance pricing relies heavily on declared values, broad property classifications, and location-based risk signals. Very little of it is based on verified, property-specific data about interior configuration, construction quality, or finish specification.

A blueprint to 3D record at inception changes the available data entirely. An insurer can now verify:

-

Actual room count and spatial layout

-

Construction and finish quality, visually confirmed

-

High-value elements: custom joinery, premium appliances, specialty fixtures, art installations

-

Structural features that affect risk: number of floors, open-plan layouts, internal staircase placement

This is the foundation of genuine risk-based pricing for residential properties. Homes with higher replacement costs can be identified and priced correctly at inception. Homes with lower-risk spatial configurations can be offered better rates. The pricing signal is grounded in verified interior reality, not self-declared estimates.

For companies like Kin, which already prices based on property-specific data signals, adding verified interior spatial records is a natural and potentially significant underwriting edge.

The Global Insurtech Opportunity

Residential property insurance is chronically underpenetrated in most markets. In the United States, approximately 6% of renters carry renter's insurance despite most leases recommending it. In India, residential property insurance penetration remains below 1% of the insurable base. In Southeast Asia, the gap is similar.

A key reason is that the product has never felt worth the friction. The onboarding is cumbersome, the value proposition is abstract, and the claims experience, when it comes, is often slow and contested.

Spatial documentation built into the policy changes the value proposition at both ends:

-

At inception: Documenting your home for insurance becomes a benefit in itself. Homeowners get a photorealistic 3D record of their property, a verified spatial inventory that has value well beyond insurance, as a renovation reference, a moving record, or a resale asset

-

At claims time: The process becomes faster, more transparent, and less adversarial. Homeowners with a pre-loss baseline get faster settlements. That is a communicable, concrete benefit that drives both purchase intent and renewal rates

This is also a genuine product design opportunity. Insurtech companies that bundle spatial documentation into their policy offering, powered by AI interior design visualization infrastructure, are creating a differentiated product experience that traditional carriers cannot easily replicate.

Lemonade's brand promise is radical transparency. A verified spatial record at inception is, structurally, the most transparent thing an insurance product can offer. Kin's brand promise is data-native underwriting. Interior spatial data is the most complete data signal available for residential properties. The alignment between these brand positions and what Foursite and Remodroom deliver is not incidental, it is direct.

Implementation: Lower Barrier Than Expected

The barrier to implementing spatial baseline documentation is lower than most insurance product teams expect. It does not require:

-

Mandatory field surveys or site visits

-

Proprietary hardware, sensors, or lidar devices

-

Complex core system integrations to get started

-

High levels of homeowner technical sophistication

What it requires is a structured document collection step at inception, with the convert floor plan to 3D or photograph-to-3D conversion handled entirely on the platform side.

A natural pilot structure for any insurer exploring this:

-

Segment: New residential policies in the $500,000+ property value tier, or policies tied to new home purchase transactions where floor plan documentation already exists

-

Duration: 6 months

-

Metrics: Claims cycle time, fraud detection rate, assessment cost per claim, customer satisfaction scores

-

Comparison: Documented vs. undocumented policies in the same cohort

The data from a pilot of this structure would produce a compelling case for broader rollout, and a defensible ROI for spatial documentation as a standard underwriting input.

Spatial Clarity Is a Risk Management Foundation

The insurance industry has spent decades building better actuarial models, better pricing algorithms, and better fraud detection systems. All of them are ultimately limited by the quality of the underlying property data.

Companies like Lemonade, Kin, and Fidelity are already operating at the frontier of what is possible with the property data that currently exists. AI interior design renders and spatial modeling tools like Foursite and Remodroom are the next layer: verified, photorealistic, queryable records of what a home actually contains, captured before loss, and available at claims time.

The insurers who build spatial documentation into their onboarding process now will have a data advantage that compounds with every policy they write. The ones who wait will continue resolving claims the same way they do today: manually, slowly, and with inadequate evidence.

Spatial clarity is not a product feature. It is a risk management foundation.

Want to explore how Foursite and Remodroom can integrate into your property documentation workflow? Write to us: reachus@virtualspaces.tech

Recommended for you

July 29, 2026

Kitchen and Bath: The Two Rooms That Decide Resale | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

July 27, 2026

Why Empty Rooms Don't Sell: Virtual Staging | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

July 24, 2026

The Quiet Sustainability Win of Deciding in 3D | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

July 22, 2026

Why Paint Swatches Lie: Test Color in 3D First | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

July 20, 2026

Why Every Home Should Be Seen Before It's Built | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

July 17, 2026

Why Big AI Labs Won't Build Floor Plan to 3D | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

July 15, 2026

How We Solve Floor Plan to 3D, Accurately | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

July 13, 2026

Designing Homes That Age With the People in Them | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

July 10, 2026

Designing Spaces for How Light Actually Moves | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

July 08, 2026

Designing Homes for Every Life Stage in 3D | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

July 06, 2026

Build an Interior Design Portfolio Without Clients | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

June 26, 2026

AI Interior Design: Full 3D Workflow in One Platform | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

June 24, 2026

Scope Creep in Interior Design: How AI Visualization Fixes It | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

June 22, 2026

What Buyers See on a Floor Plan: Your Biggest Sales Problem | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

June 19, 2026

Small Design Studios vs Big Firms: The AI Advantage | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

June 17, 2026

After the Mood Board: AI Interior Visualization | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

June 15, 2026

Foursite Pro Editor: Full Floor Plan Control for Designers | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

June 12, 2026

AI Interior Design: Style Any Room in Seconds with Foursite | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

June 10, 2026

Foursite: Floor Plan to 3D Walkthrough in Minutes | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

June 08, 2026

Win More Pitches With AI Renders Before the Meeting | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

June 05, 2026

From Floor Plan to Finished Room: What AI Now Makes Possible | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

June 03, 2026

The Interior Design Brief Is Broken. AI Fixes It | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

June 01, 2026

Pre-Construction Home Sales: AI Interior Visualization Guide | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

May 30, 2026

Interior Design Principles: Applied with AI | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

May 28, 2026

Designing Spaces for People, Not Blueprints | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

May 26, 2026

The Future of Interior Design: Closing the Visualization Gap with Foursite and Remodroom | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

May 18, 2026

How AI Visualization Upgrades Property Data Platforms | VirtualSpaces

HHemanth Velury

CEO & Co-FounderMay 12, 2026

Why Photoreal 3D Renders Are Replacing Mood Boards | Interior Design Client Presentations | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

May 08, 2026

From 2D Floor Plans To Living Worlds: The Spec‑Accurate 3D Engine | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

May 06, 2026

Why Furniture Brands Need AI 3D Visualization Now | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

May 4, 2026

How Property Portals Can Turn 2D Floor Plans into 3D Design Decisions | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

April 29, 2026

The Home-Fit Test: Why Square Footage Misleads | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

April 27, 2026

Designing Homes That Sell: 3D Visualization ROI Data | VirtualSpaces

HHemanth Velury

CEO & Co-FounderApril 24, 2026

What's Next: Foursite & Remodroom's New AI Features | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

April 22, 2026

AI in Architecture: Closing the 85% Exposure Gap | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

April 20, 2026

Interior Design Pricing in 2026: From Hourly to Value-Based Fees | VirtualSpaces

HHemanth Velury

CEO & Co-FounderApril 17, 2026

How Foursite and Remodroom Help Designers Win Clients | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

April 15, 2026

Designing Spaces for People: Remodroom + Foursite AI Guide | VirtualSpaces

HHemanth Velury

CEO & Co-Founder

April 13, 2026

Designing for the Way People Actually Live: How AI 3D Is Finally Closing the Gap Between Floor Plan and Reality

HHemanth Velury

CEO & Co-Founder

April 11, 2026

Design in Real Time: AI Renders in Your First Client Meeting

HHemanth Velury

CEO & Co-Founder

April 06, 2026

Why Real Estate Photography Is No Longer Enough: The Shift to Spatial-First Listings

HHemanth Velury

CEO & Co-Founder

April 03, 2026

Property Management's Hidden Weapon: AI 3D Floor Plans That Cut Vacancy Time and Raise Tenant Quality

HHemanth Velury

CEO & Co-Founder

April 01, 2026

Off-Plan and Oversubscribed: How AI 3D Visualization Is Transforming Real Estate Pre-Sales

HHemanth Velury

CEO & Co-Founder

March 30, 2026

Why Foursite Beats Generic AI Tools for Interior Design 3D Visualization

HHemanth Velury

CEO & Co-Founder

March 27, 2026

7 Tenets of Interior Design: How AI Accelerates Harmony in Residential Spaces

HHemanth Velury

CEO & Co-Founder

March 25, 2026

What Is the 3-5-7 Rule in Interior Design? Foursite's AI Guide for Residential Spaces

HHemanth Velury

CEO & Co-Founder

March 23, 2026

What Is the 70/30 Rule in Interior Design? Foursite's AI Guide for Residential Spaces

HHemanth Velury

CEO & Co-Founder

March 20, 2026

How AI 3D Visualization Is Rewriting Residential Interior Design Workflows

HHemanth Velury

CEO & Co-Founder

March 18, 2026

Beyond Marketing: How 3D Floorplans Transform FM, Retrofit Planning & ESG Operations

HHemanth Velury

CEO & Co-Founder

March 16, 2026

Why AI Companies Use Token Payments (And Why VirtualSpaces Is Returning To Fiat)

HHemanth Velury

CEO & Co-Founder

March 13, 2026

Floorplan‑Native Digital Twins: Beyond BIM for Consumer‑Ready Real Estate Experiences

HHemanth Velury

CEO & Co-Founder

March 11, 2026

The Foursite Platform Thesis: Why Floor Plans, Not Photos, Are the Next Property Software Primitive

HHemanth Velury

CEO & Co-Founder

March 09, 2026

Design Systems for Space: Building Reusable 3D Component Libraries on Top of AI Floorplan‑to‑3D Engines

HHemanth Velury

CEO & Co-Founder

March 06, 2026

How to Standardize Design Quality Across Global Projects Using AI Floorplan-to-3D Tools

HHemanth Velury

CEO & Co-Founder

March 04, 2026

From CAD-First to AI-First: Reskilling Your Team for AI-Native Design Workflows

HHemanth Velury

CEO & Co-Founder

March 02, 2026

Algorithmic Ergonomics Meets Photorealistic 3D: Designing Human-Centered Smart Homes with Foursite in 2026

HHemanth Velury

CEO & Co-Founder

February 27, 2026

The Ethics of AI in Interior Design: Ownership, Originality, and Client Transparency

HHemanth Velury

CEO & Co-Founder

February 25, 2026

Designing with Empathy: Using AI 3D Visualization to Improve Client Communication and Emotional Clarity

HHemanth Velury

CEO & Co-Founder

February 23, 2026

From Tool to Infrastructure: AI Floorplan-to-3D and the Next Wave of PropTech

HHemanth Velury

CEO & Co-Founder

February 20, 2026

AI Interior Design for Holiday Homes: Turn Spare Flats into High-Demand Short-Stay Rentals with 3D Visuals

HHemanth Velury

CEO & Co-Founder

February 18, 2026

The Pre‑Purchase Power Play: How Savvy Home Buyers Use 3D Floor Plan Visualization to Negotiate Better Deals

HHemanth Velury

CEO & Co-FounderFebruary 16, 2026

AI Interior Design for Non‑Designers: How Homeowners Can Brief Like Pros

HHemanth Velury

CEO & Co-Founder

February 13, 2026

Scaling a Design Business Without Hiring a 3D Team: An Owner's Guide

HHemanth Velury

CEO & Co-Founder

February 11, 2026

From Bland to Bold: How to Rescue Builder-Grade Interiors on Any Budget

HHemanth Velury

CEO & Co-Founder

February 6, 2026

The Psychology of Space: How Room Dimensions Influence Interior Design Decisions

HHemanth Velury

CEO & Co-Founder

February 4, 2026

The Future of Interior Design Visualization: How AI Technology is Transforming 2D Concepts Into 3D Reality

HHemanth Velury

CEO & Co-Founder

February 2, 2026

AI Interior Décor: How Artificial Intelligence Generates Design Options from Your Floor Plan

HHemanth Velury

CEO & Co-Founder

January 30, 2026

Photoreal vs. Reality: What Clients Actually Expect from Interior Design Visualization

HHemanth Velury

CEO & Co-Founder

January 28, 2026

The Design Approval Conversation That Changes Everything: Communication Strategy When Using Photorealistic Visualization

HHemanth Velury

CEO & Co-Founder

January 25, 2026

Interior Design as Experience Design: How 3D Visualization Changes Your Professional Identity

HHemanth Velury

CEO & Co-Founder

January 23, 2026

The Professional Gap: How 3D Visualization Changes Interior Design Client Perception

HHemanth Velury

CEO & Co-Founder

January 21, 2026

Why Clients Fire Designers (And How 3D Visualization Could Have Saved the Project)

HHemanth Velury

CEO & Co-Founder

January 16, 2026

Blueprint to Vision: Why Seeing Is Believing in Interior Design

HHemanth Velury

CEO & Co-Founder

January 14, 2026

The Speed of Responsiveness: How AI Visualization Tools Make You Look Like You Care More

HHemanth Velury

CEO & Co-Founder

January 12, 2026

Why Interior Designers and Architects Can't Compete Without AI 3D Visualization Tools

HHemanth Velury

CEO & Co-Founder

January 07, 2026

From "Saved" to "Sold": How Homeowners Are Planning Renovations with AI

HHemanth Velury

CEO & Co-Founder

January 05, 2026

The Interior Designer's Secret Weapon: Speed as Premium Positioning

HHemanth Velury

CEO & Co-Founder

December 31, 2025

Gratitude, Growth & Game-Changing Innovation: VirtualSpaces' 2025 Journey & What's Coming in 2026

HHemanth Velury

CEO & Co-Founder

December 29, 2025

Why Interior Designers Are Switching to AI Floor Plan-to-3D Tools in 2026

HHemanth Velury

CEO & Co-Founder

December 26, 2025

AI Virtual Staging for Real Estate Agents: Sell More Homes Faster with Foursite

HHemanth Velury

CEO & Co-Founder

December 24, 2025

Why Architects Are Switching to AI 2D-to-3D: The SketchUp Alternative

HHemanth Velury

CEO & Co-Founder

December 22, 2025

Cut 3 Weeks from Real Estate Sales Cycle: The ROI of AI 2D to 3D Visualization

HHemanth Velury

CEO & Co-Founder

December 19, 2025

2D Floor Plans Are Dying: Why 3D Visualization & AI Virtual Staging Are the Future

HHemanth Velury

CEO & Co-Founder

December 17, 2025

Virtual Staging vs Physical Staging: How AI Saves Money Per Property

HHemanth Velury

CEO & Co-Founder

December 15, 2025

AI Floor Plan to Image: Revolutionizing Real Estate Marketing for Agents

HHemanth Velury

CEO & Co-Founder

December 12, 2025

Color of the Year 2026: Cloud Dancer | VirtualSpaces AI Interior Design Guide

HHemanth Velury

CEO & Co-Founder

December 10, 2025

AI Floor Plan to 3D: The New Standard for Interior Design Workflows

HHemanth Velury

CEO & Co-Founder

December 08, 2025

How Interior Design Studios Can Operationalize AI 2D-to-3D Workflows (Without Breaking Their Process)

HHemanth Velury

CEO & Co-Founder

December 06, 2025

How to Implement AI Interior Design Workflows in Your Studio

HHemanth Velury

CEO & Co-Founder

December 4, 2025

How Homeowners Can Use AI Interior Design Tools to Plan Renovations with Confidence

HHemanth Velury

CEO & Co-Founder

November 28, 2025

Interior Designers in the Age of AI: From Threat Narrative to Superpower

HHemanth Velury

CEO & Co-Founder

November 21, 2025

Foursite Launch: Embracing 'Release Early, Release Often'

HHemanth Velury

CEO & Co-Founder

November 13, 2025

Foursite by VirtSpaces: Empowering Interior Designers, Architects, and Homeowners

HHemanth Velury

CEO & Co-Founder

November 7, 2025

Reimagining Architectural Education: How AI Floorplan-to-3D Technology Can Transform Design Learning

VVirtualSpaces Research Labs

AI Research Initiative

October 27, 2025

Archisculpt AI: Turning Architectural Drawings into Photorealistic 3D Spaces

AAbhijeet Naik

Co-Founder & CTO

October 13, 2025

Home Makeover: From Floor Plan to Dream Space with AI

HHemanth Velury

CEO & Co-Founder

October 6, 2025

Real-Time Rendering & AI: Revolutionizing Interactive Property Walkthroughs with VirtSpaces

HHemanth Velury

CEO & Co-Founder

September 26, 2025

Foursite - A True AI-Native Experience in Design Visualization

AAbhijeet Naik

CTO & Co-Founder

September 18, 2025

Why PropTech Startups Are Betting on AI Interior Design

HHemanth Velury

CEO & Co-Founder

September 11, 2025

How AI Differs from Traditional 3D Rendering Software

HHemanth Velury

CEO & Co-Founder

September 2, 2025

From Client to Investor: How Nila Spaces and VirtSpaces Are Redefining Proptech with AI

HHemanth Velury

CEO & Co-Founder

August 25, 2025

VirtSpaces From Virtual Reality to AI – Transforming Real Estate Visualization.

HHemanth Velury

CEO & Co-Founder

We help teams collaborate seamlessly and reduce costs. Virtual Spaces offers cutting-edge technology with flexible plans designed to fit modern teams.

Copyright © VirtSpaces Pvt. Ltd. 2025 All Rights Reserved.

CIN: U74999KA2016PTC094921